How to Shop for Medicare Insurance: A Step-by-Step Guide

Article at a glance

The most important part of shopping for Medicare insurance is understanding each of the options available.

Reflecting on past insurance plans and current desires for a health insurance plan is crucial when picking the right plan.

Since there are so many Medicare insurance options to choose from or combine, comparing plans can aid a patient with their decision.

Before most Americans turn 65, they become eligible to enroll in the Federal Medicare Program. Medicare is a federal health insurance program provided by the United States government for U.S. citizens age 65 and older as well as certain younger citizens with disabilities or end-stage rental disease (ESRD).

Before enrolling in a Medicare plan, it is important to know all the options available, and there are plenty of plans and combinations to choose from to be sure. As such, figuring out which Medicare plan is best can be an overwhelming decision to make.

Luckily, there are a number of steps future beneficiaries can take to pick the most optimal Medicare plan for themselves. Read on below to learn more about the steps Medicare enrollees should take to make the enrollment process as smooth and stress-free as possible.

Step One: Understand How Medicare Works

Before diving into all the different options, it’s important to understand the structure of the Federal Medicare Program. This will help make navigating Medicare enrollment that much easier.

Medicare is broken into three parts, each one designated to cover certain health care services and costs. These Medicare Parts include:

Medicare Part A (hospital insurance)

Medicare Part B (medical insurance)

Medicare Part D (prescription drugs)

Medicare Part A provides hospital insurance, e.g., inpatient hospital care, home healthcare, nursing home care, and hospice care.

Medicare Part B offers medical insurance for necessary medical or preventive care services such as vaccinations, outpatient check-ups and procedures, mental health screenings, durable medical equipment (DME), and more.

Finally, Medicare Part D provides prescription drug coverage. There are various Medicare prescription drug plans to choose from to help cover prescription drug costs.

Step Two: Research The Different Types Of Medicare Plans

There are various Medicare plans to choose from, some that can even be combined to get an enrollee the most comprehensive coverage possible. However, the two main ways to get Medicare coverage include Original Medicare or Medicare Advantage (Medicare Part C).

Medicare Supplement Insurance (Medigap) is also available as additional coverage for Original Medicare. Some Americans are also eligible for both Medicare and Medicaid coverage. This is known as Dual Eligibles.

Note: Because a Medicare Advantage plan is considered to be a type of Medicare Supplement Insurance, Medicare Advantage beneficiaries are not eligible for additional Medigap insurance or to additionally enroll in a Dual Eligibles program.

Original Medicare

Original Medicare consists of Medicare Part A and Medicare Part B. Original Medicare does not include Medicare Part D, which means Original Medicare enrollees would need to add on a Medicare prescription drug plan separately in order to get coverage for prescription drugs.

Medicare Advantage

Medicare Advantage (MA) plans are Medicare-approved health insurance policies from private insurance companies that aim to offer more comprehensive medical coverage within Medicare. MA plans bundle Medicare Part A and Medicare Part B into one insurance plan. Many Medicare Advantage plans also include Part D coverage within their policies as well.

Most Medicare Advantage plans also often include additional benefits including coverage for dental, vision, and hearing.

There are various types of MA plans available, each one providing different benefits and including distinct networks of providers and hospitals. Health Maintenance Organization (HMO) plans and Preferred Provider Organization (PPO) plans are the two most common types that are chosen.

Note: To learn more about MA plan types and the pros, cons, and overall differences between them, visit this source.

Medicare-Medicaid (Dual-Eligibles)

Medicare and Medicaid differ in the sense that Medicare is a federally funded health program for seniors or those with disabilities and Medicaid is a state-funded health program for lower-income households. That being said, these insurance programs can be combined for a patient and are commonly called “dual-eligibles.”

When they are paired together, Medicare takes place as primary insurance while Medicaid functions as secondary insurance. This plan includes no premiums while offering Parts A, B, and D coverage in addition to various benefits such as insurance for dental, vision, and hearing. However, in order to select this plan, one must qualify for Medicaid coverage.

Note: To find out more on qualifying for Medicaid and see if you’re eligible, visit this source.

Medicare Supplement Insurance Plans

Medicare Supplement Insurance, commonly called “Medigap” or “MedSupp,” is sold by private insurance companies to help patients cover the gaps in Original Medicare insurance. Medigap typically comes with higher monthly premiums than Medicare Advantage plans.

Step Three: Outline Insurance Wants and Needs

Once options are laid out and understood, it’s time for a patient to reflect on which aspects they want and need out of an insurance plan.

To start, enrollees need to make sure any preferred health care providers (doctors, specialists, nurses, etc.) accept the insurance plan they’re leaning towards. Furthermore, they need to think through past insurance plans and their pros and cons. Doing so will help a patient to see what their past plans were lacking in or succeeded at, thus helping them understand what they desire out of an insurance plan now.

The following questions can help narrow down the right Medicare plan:

How much are monthly out-of-pocket costs for the plan? Is this in their budget?

What should the deductible be?

Does a package deal of prescription drug coverage, dental insurance, vision insurance, and added benefits hold importance to the enrolee?

Does the enrollee qualify for Medicaid, thus being eligible for a dual-eligible plan?

Are their preferred healthcare providers and hospitals included in-network?

Is transportation to and from the provider’s office necessary? Confirm whether transportation is included in the plan.

Is it important for the plan to include mental health and well-being benefits?

What medications are covered? Whether you have a Part D Plan or an MA plan that includes prescription drug coverage, it’s important to make sure your medications are covered.

Step Four: Compare Options

Once ideal insurance plans are narrowed down, the patient should compare their options in order to decide which Medicare plan is right for them. If they are struggling to find plans in their area or simply want to compare insurance plan options, visit one of the sources below:

Step Five: Speak With an Insurance Agent

Insurance can be tricky and confusing to understand. If further assistance is required or questions are left rattling inside a patient’s brain, they should speak with a licensed insurance agent at an insurance company, Medicare, or otherwise.

Even if a patient feels like they have a strong, general understanding of their options and which plan is right for them, it’s good to speak with an agent to ensure they know what they’re signing up for.

To schedule a time to talk with a Medicare insurance agent, visit one of the sources below:

Note: One of the benefits of Oak Street Health is that they have agents ready and available to talk any patient through their Medicare plan benefits. If a patient ever needs a refresher on what their plan offers, schedule a call with an Oak Street Health provider.

Step Six: Enroll In Medicare

The final step in shopping for a Medicare insurance plan is purchasing a plan. Visit the government’s Medicare website to do so.

While most are automatically enrolled in Medicare during their Initial Enrollment Period (IEP), some may still need to sign up. The application can be accessed here.

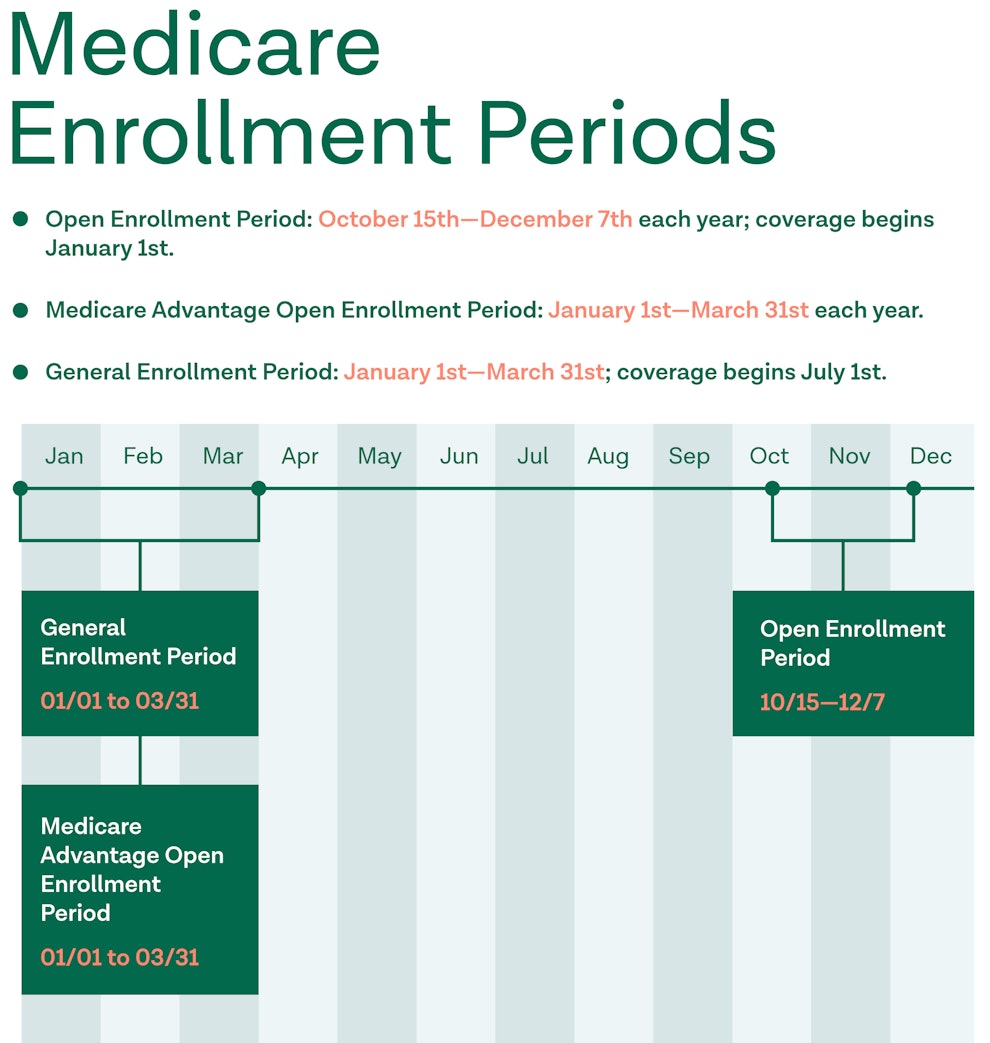

Note: Learn more about enrolling in Medicare at this resource, as well as mistakes to avoid during open enrollment at this resource.

Who is the best person to talk to about Medicare?

Medicare customer support representatives are available to talk 24/7 at:

1-800-MEDICARE (1-800-633-4227); TTY users should call 1-877-486-2048

Live Chat on Medicare.gov

For more information on talking about Medicare, visit this source.

How do I sign up for Medicare?

Most people are automatically enrolled in Medicare Part A when they are approved for their Social Security or Railraod Retirement Board benefits. If you’re not automatically enrolled, you can sign up for Medicare online on Social Security’s website at this source.

Sources

https://www.medicare.gov/what-medicare-covers/what-part-a-covers

https://www.medicare.gov/what-medicare-covers/what-part-b-covers

https://www.medicare.gov/drug-coverage-part‑d/what-medicare-part-d-drug-plans-cover

https://www.hhs.gov/answers/medicare-and-medicaid/what-is-medicare-part‑c/index.html

https://www.medicare.gov/supplements-other-insurance/whats-medicare-supplement-insurance-medigap

https://www.medicare.gov/what-medicare-covers/your-medicare-coverage-choices

https://www.medicare.gov/plan-compare/#/coverage-options/?year=2022&lang=en

Become a patient

Experience the Oak Street Health difference, and see what it’s like to be treated by a care team who are experts at caring for older adults.